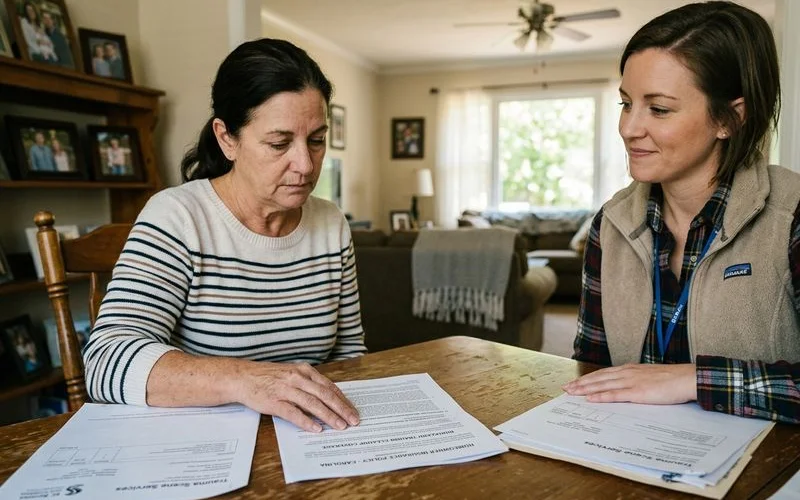

From what I see in the field every day, the first question families ask during a crisis is always about the financial impact. The emotional weight of an unattended death is heavy enough without worrying about how to pay for professional remediation. That added financial stress often feels completely overwhelming for families already dealing with a difficult situation.

Does Insurance Cover Trauma and Biohazard Cleanup in South Carolina?

Fortunately, many standard HO-3 homeowner policies in our state actually provide coverage for these specialized services. The short answer is usually yes, but the specific details depend entirely on your carrier and the exact language in your policy.

Our trauma and unattended death cleanup crew at Summerville Hoarding Cleanup regularly advocates for families across the Charleston metro area and the wider Lowcountry. Dealing with bureaucratic paperwork is the absolute last thing you need right now. The data behind these claims provides a clear path forward, allowing us to explain how insurance companies classify this work and outline exactly how to get your cleanup funded.

Does Insurance Cover Trauma and Biohazard Cleanup in South Carolina?

Biohazard cleanup does not usually have a dedicated line item on a standard South Carolina property policy. Instead, the costs fall under one or more existing provisions within your contract. Finding the right category is your first step toward getting the bill paid.

Dwelling Coverage (Coverage A)

Your primary dwelling provision protects the physical structure of your house. Removing and replacing contaminated building materials like drywall or subflooring typically falls into this specific bucket. This path represents the most common way to fund an unattended death remediation project.

Our team sees this coverage applied frequently when bodily fluids compromise the actual architecture of the building. The average South Carolina home carries around $300,000 in dwelling protection. That amount leaves plenty of room to cover the structural tear-out and rebuilding costs.

Here are the typical structural components covered under this section:

- Contaminated wall-to-wall carpeting and padding

- Biological fluid seepage into wooden subflooring

- Affected drywall and baseboards

- Compromised insulation behind walls

Personal Property Coverage (Coverage C)

If biological matter ruins your furniture, mattresses, or clothing, your personal property provision applies. This section reimburses you for the items you must throw away. Standard HO-3 policies usually set this limit at 50% to 70% of your total dwelling coverage.

You will need to check if your policy offers Actual Cash Value or Replacement Cost Value. The difference dictates how much money you receive.

| Valuation Type | How It Works | Financial Impact |

|---|---|---|

| Actual Cash Value (ACV) | Pays the depreciated value of the item today. | You receive less money for older furniture. |

| Replacement Cost Value (RCV) | Pays what it costs to buy a brand new equivalent item. | You receive enough to fully replace the lost item. |

Additional Living Expenses (Coverage D)

Severe scenes often make a house completely uninhabitable for several days. Your policy includes a loss of use provision to pay for temporary housing and meals during the project. Insurers in our state typically cap this allowance at 20% of your main dwelling limit.

We regularly help families secure temporary lodging while we work. A policy with a $300,000 structural limit would provide up to $60,000 for these displacement costs. This budget allows you to stay in a comfortable hotel rather than sleeping in an unsafe environment.

Liability Coverage

Landlords and property managers often rely on their liability provisions to handle these unexpected bills. This section protects property owners if someone is injured or if a tenant causes a severe biohazard event. Standard limits usually start at $100,000 and can be increased easily.

Property owners facing a hoarding situation left behind by a tenant should review this section immediately. The liability umbrella often catches the costs that standard property damage clauses exclude.

What Insurance Typically Covers

Based on extensive field work with local carriers like State Farm and Farm Bureau SC, we know exactly what adjusters look for. You need to present a highly specific list of expenses.

Generally Covered Items

Professional remediation labor is almost always an approved expense. The national average cost for these specialized services ranges between $1,000 and $4,000 per affected room. Adjusters understand that regular maid services cannot safely handle biological pathogens.

Our technicians strictly follow Occupational Safety and Health Administration (OSHA) protocols during every project. This compliance is a major reason why carriers approve our invoices.

Standard approved costs usually include:

- Certified technician labor rates

- Hospital-grade antimicrobial chemicals

- Red bag biohazardous waste disposal fees

- Structural tear-out of compromised materials

Sometimes Covered (Depends on Policy)

If a decomposition event happens while the air conditioner is running, the ductwork often becomes contaminated. Cleaning the HVAC system according to National Air Duct Cleaners Association (NADCA) standards is sometimes approved. You will need to prove the airborne contamination is a direct result of the primary event.

Environmental consultant fees are another gray area. Hiring an industrial hygienist to verify the cleanliness of the home might require special approval from your desk adjuster.

Typically Not Covered

Carriers draw a hard line at damage that existed before the traumatic event occurred. Mold damage provides the best example of this exclusion in our humid coastal environment. Standard homeowner contracts exclude mold growth unless you can prove it resulted directly from the recent incident.

We always warn clients about the negligence clause. If an adjuster determines you failed to maintain the property over several years, they will likely deny the cleanup of that long-term mess.

The Claims Process Step by Step

Filing a claim requires specific documentation and a clear timeline. Following a strict sequence prevents unnecessary delays and frustrating denials.

Step 1: Notify Your Insurance Company Immediately

You must contact your provider as soon as you discover the situation. South Carolina Code Section 38-59-20 requires insurers to handle claims with reasonable promptness and avoid improper delays. Initiating the process quickly locks in your right to a timely response.

Our office suggests keeping your initial phone call brief and factual. Provide the police report number, the date of discovery, and your policy details. Save the detailed explanations for the field adjuster later.

Step 2: Document Everything

Do not enter a contaminated room just to take pictures. Your assigned safety team will document the worst areas while wearing proper protective gear. Keep a simple folder with all your hotel receipts and communication logs.

Proper photographic evidence forms the absolute foundation of your request for funding.

We strongly suggest using a timestamp camera application on your smartphone for the exterior and safe areas. This software burns the exact date, time, and GPS location into every image, which adjusters love to see.

Step 3: Get a Professional Assessment

Your assigned desk representative needs a formal, itemized estimate before they can cut a check. The report breaks down the exact square footage of drywall removal, the number of labor hours, and the volume of chemicals needed.

Our estimators use Xactimate, which is the exact same pricing software utilized by 80% of the insurance industry. Submitting an estimate in their native language speeds up the approval timeline significantly.

Step 4: Work With the Adjuster

Your carrier will assign a specific person to investigate your file. You might deal with a staff adjuster who works directly for the company, or an independent contractor hired for overflow work. Independent representatives often process these severe cases faster because they handle high volumes of catastrophic damage.

Our staff communicates directly with these representatives every single day. The conversations focus on answering technical questions and explaining why specific actions are biologically necessary.

Step 5: Authorize the Work

Emergency mitigation can often start before the final paperwork is fully signed. If the house is actively deteriorating, carriers will authorize immediate stabilization to stop the damage from spreading. You will typically sign an Assignment of Benefits (AOB) form at this stage.

The Assignment of Benefits (AOB) form provides three main benefits:

- Allows the contractor to bill the carrier directly

- Removes you from the middle of complex financial transactions

- Accelerates the start of emergency mitigation

Step 6: Submit Final Documentation

After the final wipedown, you must prove the house is actually safe for human habitation. Scientific validation is the only way to close the file completely.

We use Adenosine Triphosphate (ATP) testing meters to prove the absence of biological matter.

| Test Result | Relative Light Units (RLU) | Action Required |

|---|---|---|

| Pass | Under 10 RLU | Surface is safe and sterile. |

| Caution | 11 to 29 RLU | Area requires a second cleaning pass. |

| Fail | 30+ RLU | Surface is highly contaminated. |

Special Considerations for South Carolina

Our unique coastal environment changes how carriers handle property damage. You must understand local regulations to maximize your payout.

Humid Climate Complications

The Lowcountry experiences average humidity levels well above 70% for most of the year. This heavy moisture accelerates organic decomposition dramatically.

Mold spores can bloom across a compromised room in less than 48 hours under these conditions.

Our fast response times are critical here. If you delay the initial phone call, the desk representative might argue that you allowed preventable secondary mold damage to occur.

Hurricane and Flood Considerations

Standard property contracts explicitly exclude water rising from the ground. If a biohazard event is complicated by a severe coastal storm, the situation requires two separate claims. You will need to engage your National Flood Insurance Program (NFIP) policy for the water damage portion.

We help property owners separate these overlapping issues. Properly categorizing the damage prevents automatic denials from your primary carrier.

State Consumer Protection Laws

You have strong legal rights if a company treats you unfairly during this process. The South Carolina Department of Insurance strictly regulates how these corporations must behave. By state law, an insurance entity has exactly seven days to respond to an official Department of Insurance complaint.

State statutes also require companies to pay undisputed claims within 90 days of a formal demand.

We monitor these deadlines closely to ensure your project stays fully funded.

When Hoarding Is Involved

Combining a traumatic event with severe clutter creates a massive administrative headache. Carriers view these complex environments very differently than an empty, clean house.

The Pre-Existing Condition Challenge

Most desk representatives view severe clutter as a major liability risk and a pre-existing condition. Industry professionals use the Institute for Challenging Disorganization (ICD) Clutter-Hoarding Scale to measure severity. Homes rating a Level 3, 4, or 5 on this scale almost always trigger pushback from adjusters.

Our priority is proving that the biological hazard resulted from a sudden, covered incident. The company must pay to clean up the recent trauma, even if they refuse to pay for hauling away decades of accumulated newspapers.

Strategies for Hoarding-Related Claims

The secret to getting these dual-issue files approved is strict line-item segregation. Presenting clear, separated data stops the adjuster from rejecting the entire project outright. This strategy secures funding for the most expensive, hazardous portion of the work.

We write two completely separate estimates. One document details the biological decontamination, and the other covers general trash removal.

Understanding Your Policy Before You Need It

Waiting until a crisis happens is the worst time to read your contract. A quick review today can save you thousands of dollars tomorrow.

Review Your Policy Now

Pull your paperwork out of the filing cabinet and find your declarations page. You need to verify your Coverage A structural limits and your exact deductible amount.

Look specifically for these key details:

- Coverage A structural limits

- Exact deductible amounts

- Written exclusions regarding biological waste

- Clauses detailing long-term neglect

Our experience shows that many homeowners are dangerously underinsured for severe interior damage. Checking your limits takes ten minutes and provides massive peace of mind.

Ask Your Agent Specific Questions

Call your local agent and ask them a direct, specific question. Do not ask a vague question about general cleaning. You need to ask, “Does my current HO-3 form explicitly cover unattended death remediation and biohazard removal?”

Write down the exact date you called and the name of the person who answered. This log protects you if they give you incorrect information over the phone.

Consider Supplemental Coverage

If your current contract excludes these events, you can usually buy a specific rider. Adding a dedicated biohazard endorsement is surprisingly affordable. The premium increase often costs less than $100 per year.

This tiny investment provides a massive safety net. Paying out of pocket for a $4,000 sanitation project is devastating for most families.

How Summerville Hoarding Cleanup Helps With Insurance

Managing an active crisis while fighting with a corporation is an impossible task.

Our administrative team takes over the entire communication loop for you. Here is exactly how we handle the corporate side of your project:

- Drafting Xactimate estimates that match standard industry formatting

- Submitting timestamped photographic evidence directly to the portal

- Providing scientific ATP swab results to prove successful sterilization

- Filing supplemental requests if we uncover hidden structural damage

- Negotiating directly with the assigned field investigator

We hold strong working relationships with all the major carriers operating in the Lowcountry. This familiarity means we know exactly what formatting State Farm requires versus what Allstate expects. Our deep understanding of these specific preferences drastically reduces processing times for our clients.

Taking the First Step

If you need immediate help in Charleston, Summerville, or anywhere in the Lowcountry, do not wait to take action. Does Insurance Cover Trauma and Biohazard Cleanup in South Carolina? Yes, and we are ready to help you prove it.

You need to call your agent to start the paperwork, and then you need to call our dispatch team at (843) 517-7097 for a formal assessment.

Our estimators will generate the exact technical documentation your carrier demands. A dedicated project manager stands right beside you during every single inspection and phone call. Your only job right now is taking care of your family, so let us handle the heavy lifting and the corporate negotiations.

Delaying this work only makes the environment more dangerous and the final bill more expensive. Pick up the phone today and let our specialists build a solid, data-driven plan for your property.